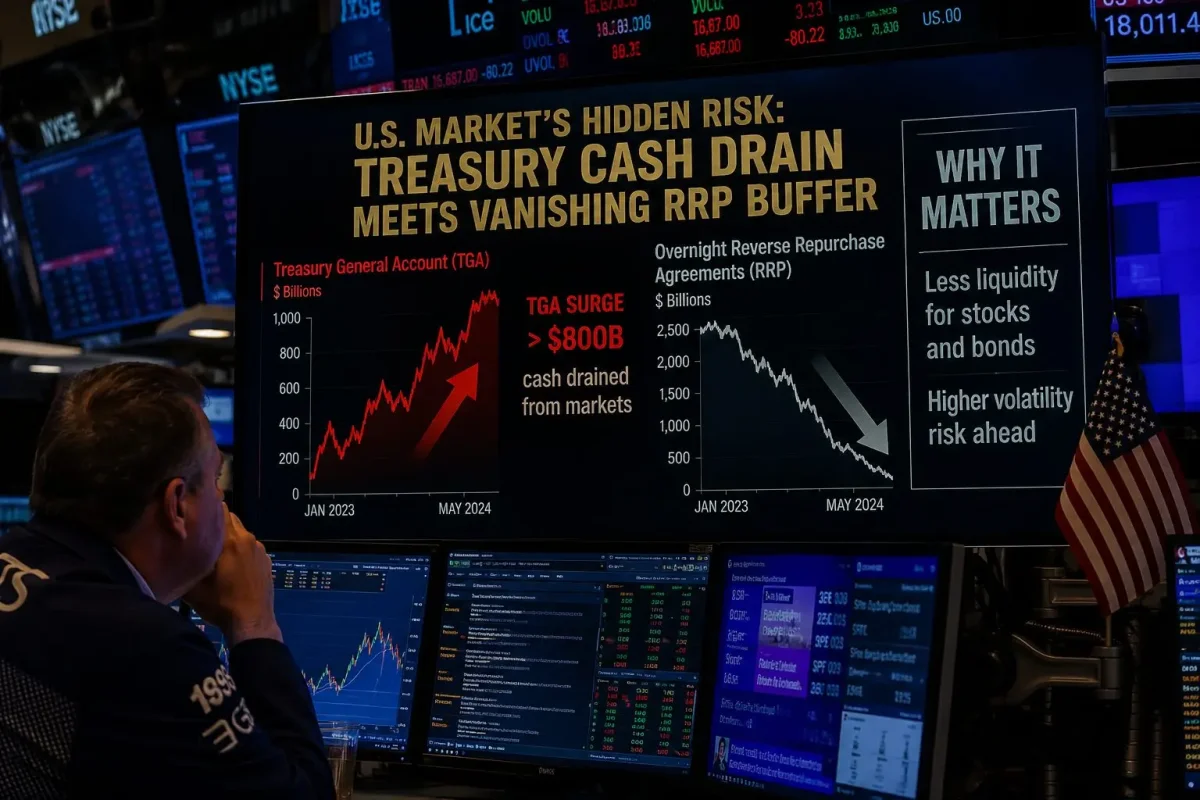

New York, July 2, 2026, 14:20 EDT — U.S. equity markets are open for trading Thursday but will close Friday for Independence Day, while bond markets followed SIFMA guidelines with an early 2 p.m. EDT close. The data that has captured the attention of market professionals, however, is not the holiday schedule but the increasingly thin cash buffer underpinning Treasury securities.

The Federal Reserve's overnight reverse repo (ON RRP) facility took in just $2.175 billion on July 2, down sharply from recent months. At the same time, the Treasury General Account (TGA) stood at $919.14 billion as of June 30. Based on these latest figures, the RRP cushion represents only 0.24% of Treasury cash—a historically low level that raises the risk of funding market stress.

This is not necessarily a stress print on its own, but it creates a soft setup. The Treasury is about to boost its cash pile and increase bill issuance, while bank reserves are already declining. The latest Fed data show reserve balances with the Fed averaged $2.951 trillion in the week ending July 1, down $82 billion week over week. Even a small move in funding rates can spill into stocks through yields and leverage.

Goldman Sachs Group (NYSE: GS) client data reviewed by Reuters indicates fundamental long-short hedge funds are up 17.4% so far this year, posting their best quarter since Goldman began tracking. However, the funding link is hard to overlook. If rates and funding tighten simultaneously, de-grossing could come fast, especially for heavily owned tech stocks.

Fed Chair Kevin Warsh on Wednesday warned that balance sheet risk is back in focus. He stated that any decisions would be "well deliberated publicly" and that the Fed would wait until markets understood them before taking action. The Fed's balance sheet currently stands at $6.7 trillion, down from its $9 trillion peak in 2022 but still above the $4.2 trillion level seen before the pandemic.

Kay Haigh, global head and CIO of fixed income and liquidity solutions at Goldman Sachs Asset Management, noted that the Fed remains focused on inflation readings since the labor market is holding steady. Any upside surprise could mean a rate hike comes sooner. Cash data is key, Haigh said, because markets could take a hit from inflation driving rates up while simultaneously facing a funding squeeze from heavier bill supply.

The Treasury is looking for $671 billion in privately held net borrowing for July-September and wants an end-September cash pile of $950 billion. The TGA could top out close to $1 trillion, give or take $50 billion, in late July. Treasury has indicated that bill auction sizes should increase in July. Repo markets have become so quiet that the current calm is itself seen as a risk. Lou Crandall, chief economist at Wrightson ICAP, told Reuters on June 30 that he foresaw "normal turn-of-the-quarter pressures but nothing disruptive." The quarter-end passed without any blowout moves.

Stocks moved on jobs data Thursday. The Bureau of Labor Statistics reported June payrolls increased by 57,000, unemployment came in at 4.2%, and participation slipped to 61.5%. Jobs fell in leisure and hospitality. According to Reuters, the Dow gained 0.7%, the S&P 500 was flat, and the Nasdaq dropped 0.6%. The Philadelphia chip index sank 4.1% after tumbling 6.3% Wednesday.

Florian Ielpo, head of macro at Lombard Odier Investment Managers, called the jobs report "the best number we could hope for," saying the labor market isn't hot enough to push inflation higher. Ellen Hazen, chief market strategist at F.L. Putnam Investment Management, highlighted the sharp drop in the labor force as the main issue. The thin cash buffer under Treasuries, however, remains the risk that is not getting much attention ahead of the holiday.