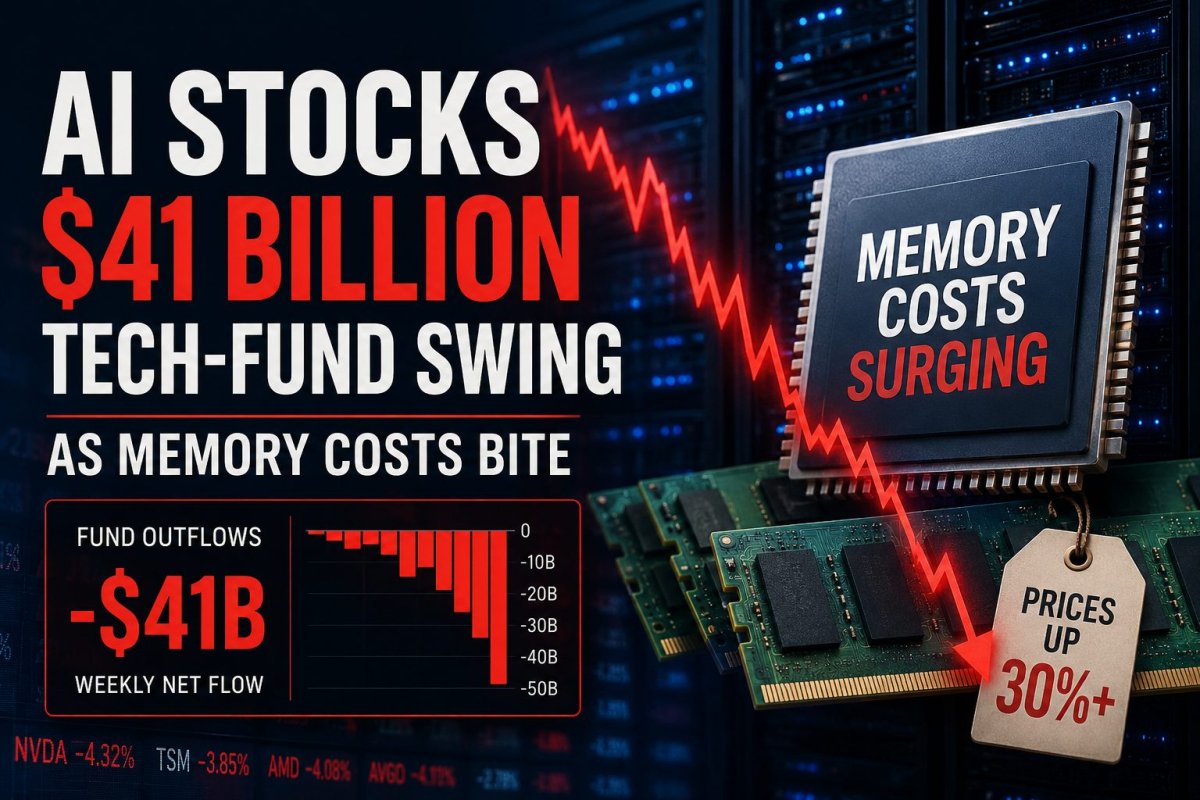

NEW YORK, June 27, 2026 — Technology sector funds experienced a dramatic reversal in investor sentiment during the week ended June 24, with nearly $20 billion in outflows erasing the prior week's $21.46 billion in inflows, according to LSEG Lipper data cited by Reuters. The $41 billion swing in just two weeks preceded a sharp sell-off in chip stocks that dragged the Nasdaq down 4.6% and sent the Philadelphia semiconductor index to its worst weekly performance since April.

The broad market showed a stark split: the S&P 500 fell 2% for the week, while the Dow Jones Industrial Average managed a 0.6% gain and the Russell 2000 rose 1%. The divergence underscores a rotation out of AI and technology names, even as the rest of the market held relatively steady. The Philadelphia semiconductor index closed down 5.3% on Friday alone, bringing its weekly loss to 7.9% — the steepest since early April.

David Stubbs, chief investment strategist at AlphaCore Wealth Advisory, told Reuters that lingering concerns over "profitability and the capex story" continue to weigh on the sector. Investors are questioning whether the massive capital expenditures required for AI infrastructure will translate into sustainable returns.

Micron Technology (NASDAQ: MU) reported strong fiscal third-quarter results, with cloud memory and data center revenue surging to $25.29 billion, representing 61% of total sales, up from $4.92 billion a year earlier. The company forecast fourth-quarter revenue of $50 billion, plus or minus $1 billion. CEO Sanjay Mehrotra described memory as a "strategic value" in the AI era, noting that Micron continues to invest at "record levels." However, investors focused on the cost implications for buyers, as memory price increases ripple through the supply chain. Reuters reported that Apple (NASDAQ: AAPL) raised prices on iPads and MacBooks after paying more for memory and storage. "Micron's gains were 'coming out of somebody else's hide,'" said Carol Schleif, chief investment officer at BMO Family Office.

Funding pressures also emerged. Oracle (NYSE: ORCL), CoreWeave (NASDAQ: CRWV), and SoftBank Group (TYO: 9984) slipped after The New York Times reported that OpenAI may not go public until 2027, according to Barron's. OpenAI has not set a timeline, stating in a June 9 statement that "it may be a while." The news hit AI-linked stocks globally, with Kioxia Holdings (TYO: 285A) dropping 12% in Tokyo on Friday. CFO Yoshihiko Kawamura told reporters the chipmaker aims to list American depositary shares "around that time" early next financial year, which Smartkarma's Douglas Kim described as "highly confident" guidance for the next 9 to 12 months.

The upcoming week is packed with macro events and shortened by the Independence Day holiday. The Bureau of Labor Statistics will release the June jobs report on July 2 at 8:30 a.m. ET. U.S. markets will be closed on July 3 for Independence Day. Economists polled by Reuters forecast 110,000 jobs added in June. Julia Hermann, global market strategist at New York Life Investment Management, told Reuters that recent tech gains were concentrated in "memory-related equities," and she questioned whether higher interest rates could threaten those gains.