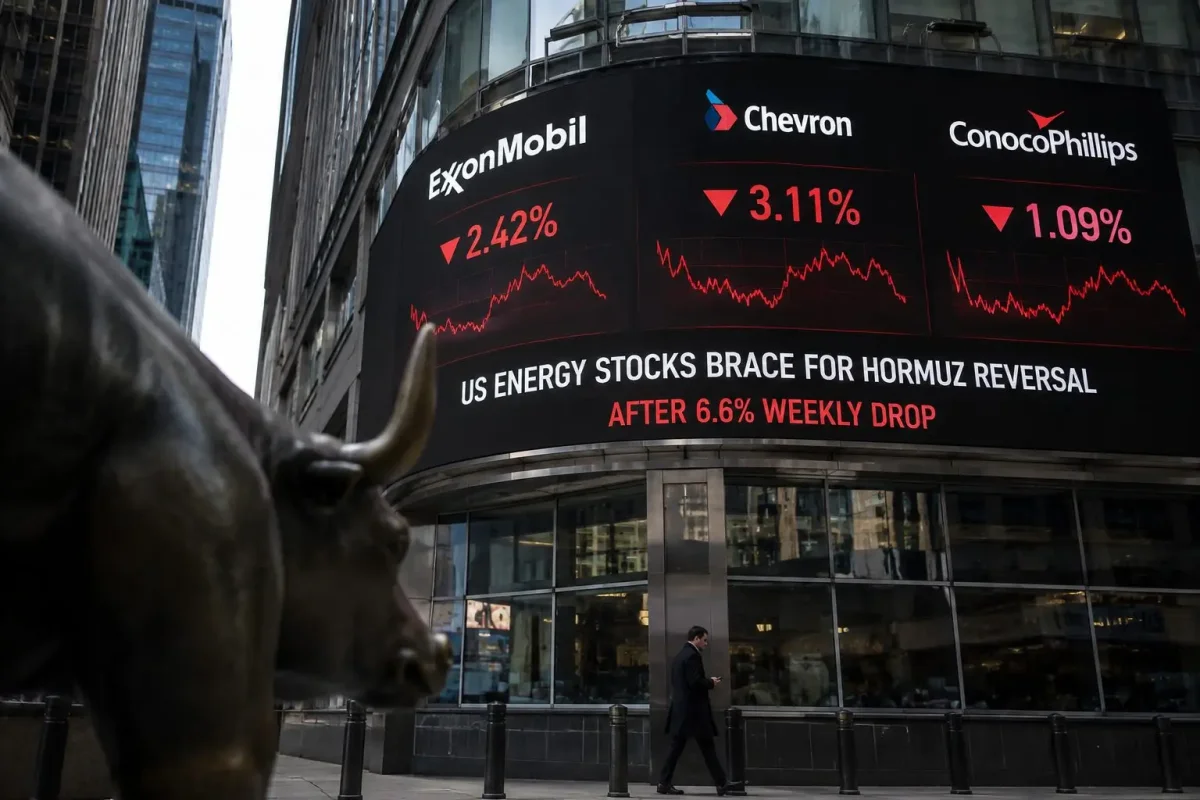

The Energy Select Sector SPDR Fund (XLE) suffered a 6.6% decline during the shortened trading week, mirroring losses across major U.S. energy companies. The sell-off was driven by a 7.7% plunge in Brent crude, which settled at $80.57 a barrel on Friday, down from June 12 levels. The global benchmark's decline was fueled by Iran's continued closure of the Strait of Hormuz, a critical chokepoint for global oil shipments.

Iran has stated that the strait will remain closed until a Lebanon ceasefire is maintained and oil-sale waivers are granted. U.S. and Iranian officials are currently engaged in talks in Switzerland, but no resolution has been reached. The closure has effectively halted tanker traffic through the strait, with no vessels passing since Tehran's latest statement, according to vessel tracking data cited by Reuters. However, the U.S. military maintains that the route remains open.

The S&P 500 energy sector dropped 6.6% over four sessions, while the broader S&P 500 index rose 0.93%. Investors had initially priced in an interim U.S.-Iran deal that would allow Gulf oil to return to the market, but the ongoing blockade has upended those expectations. 'The market was pricing in a deal and pretty seamless execution,' said Rory Johnston, founder of Commodity Context. 'That doesn't seem to be what we’re getting thus far.'

Major U.S. oil stocks were hit hard. Exxon Mobil (XOM) fell 6.3% from its June 12 close through Thursday, while Chevron (CVX) slipped 7.3% and ConocoPhillips (COP) dropped 7.9%. These declines leave the stocks vulnerable to sharp moves if crude futures rally when trading resumes on Monday. The direction of Monday's market hinges more on actual tanker traffic than on official statements, according to analysts. 'The slightest sort of disturbance is going to register in the market,' said John Kilduff, partner at Again Capital.

The supply disruption has left a significant volume of crude stranded. Kpler analyst Muyu Xu estimates that reopening the strait could release around 93 million barrels of non-Iranian crude currently waiting to pass. Goldman Sachs expects Gulf exports to return to prewar levels by the end of July, but Bank of America warns that mine-clearing operations could stretch on for months, potentially keeping the market tight through the fourth quarter. Fatih Birol, head of the International Energy Agency, described the risk starkly: 'The vase is broken.'

Oil traders are now focused on Wednesday's weekly petroleum report from the U.S. Energy Information Administration (EIA), due at 10:30 a.m. EDT. The Strategic Petroleum Reserve stands at 340.3 million barrels, the lowest since 1983, while stocks at Cushing, Oklahoma, are near minimum levels. Any further drawdown could exacerbate price volatility.

On the supply side, U.S. producers are increasing activity. The number of active oil-and-gas rigs rose to 563 last week, marking the eighth increase in the past nine weeks. The EIA forecasts U.S. crude output will reach a record 13.7 million barrels per day in 2026, which could cap prices over the longer term once Gulf shipments recover. However, the near-term outlook remains uncertain. Citi projects Brent will average $75 in Q3 and $70 in Q4 if the deal holds and tankers resume moving. But if closures persist or violence escalates, supply risk premiums will return, boosting oil stocks and reigniting inflation and interest rate concerns on Wall Street.